Affordable housing remains one of the most pressing issues in the United States. The challenge has worsened in recent years as home prices and rents have surged, pushing many families and individuals out of the market. As of 2025, some states stand out for offering more affordable housing options, helping to meet the growing demand. This article provides a detailed look at states offering the best affordable housing opportunities, considering housing costs, availability, and economic conditions.

Do you ever wonder why some people seem to accumulate wealth effortlessly while others struggle despite earning a good income? The difference often isn't luck, inheritance, or a high-paying job—it's habits. Wealthy individuals follow innovative financial practices that build their net worth gradually but consistently.

How much should you save? Where should you invest? What strategies will help your money grow while keeping risks low? Let’s break it down step by step so you can build a solid retirement portfolio that works for you.

Finding affordable housing can feel like searching for a needle in a haystack, especially in cities with high demand and rising rental prices. Many people struggle to find housing that fits their budget and needs, but with the right approach and mindset, hidden gems remain. This article will guide you through practical steps to uncover these affordable housing options, covering a range of methods beyond conventional rental listings.

In recent years, the biotech sector has gained significant attention from investors for its ability to transform healthcare and its growing potential to generate long-term returns. From gene editing to immunotherapies and personalized medicine, the breakthroughs in biotechnology are increasingly being viewed as opportunities for significant growth. As technology advances and new treatments come to market, investors are increasingly drawn to the sector, driven by both the promise of innovation and the potential for substantial returns. However, this growing interest also reflects how biotech companies are positioning themselves as key players in the future of medicine and healthcare solutions.

As we move into 2025, one of the most significant shifts in the stock market is the overwhelming dominance of AI-related stocks. From tech giants to new startups, the artificial intelligence sector is reshaping industries, redefining business models, and quickly becoming a driving force behind market performance. While AI's growth has been discussed for years, 2025 is the year it truly takes centre stage. But why exactly are AI stocks leading the charge, and what factors fuel this rise? Look deeper at the trends, innovations, and market dynamics contributing to AI's dominance.

Biometric payments are inaugurating a paradigm shift in the transactional sphere, presenting an esoteric amalgamation of inviolable security and superlative convenience. As the ubiquity of digital transactions burgeons, the exigency for impregnable and adept payment stratagems becomes paramount. Biometric payment systems security and biometric payments enhancing convenience are pioneering this metamorphosis, engendering an effortless symbiosis between consumers and enterprises.

In today's fast-paced world, financial literacy is more important than ever. It refers to the ability to understand and manage financial resources effectively. With rising living costs, fluctuating job markets, and an increasing reliance on credit, individuals must be equipped with the knowledge and skills to make informed financial decisions. Financial literacy is not just a buzzword; it is a vital component of financial security, allowing people to achieve their goals, avoid debt traps, and plan for a stable future. Let’s delve into the fundamentals of financial literacy and its significance in fostering financial security.

In 2024, blockchain technology and cryptocurrency will continue evolving, unexpectedly shaping the financial landscape. With increasing institutional interest and expanding use cases, blockchain and cryptocurrency have established a strong foothold in mainstream markets. However, alongside growth, investors must remain cautious about risks and challenges. Understanding the emerging trends in cryptocurrency investments can provide better insight into what to expect this year and beyond.

Geopolitical tensions are reshaping the semiconductor industry, one of the most critical sectors in global technology. The complex interplay between trade conflicts, government policies, and technological innovation influences the performance of semiconductor stocks. This article examines how these factors impact the industry in 2024, highlighting key trends and challenges.

Wondering what stagflation is and how it affects your wallet? Find out how to navigate this economic challenge and protect your finances. Read now!

Investing in rental properties can be a great way to build wealth and secure financial stability. However, maximizing the return on investment (ROI) requires careful planning and strategic management. Here’s a guide to help you get the most out of your rental properties in 2024.

Selecting the optimal bank account is pivotal for efficacious financial stewardship. Many individuals persist with the same bank for years, yet numerous compelling rationales exist to contemplate switching bank accounts. Whether you are pursuing augmented interest rates, diminished fees, or superior customer service, discerning the propitious moment to transition can significantly enhance your fiscal well-being. In this discourse, we shall elucidate various scenarios and stratagems to aid you in identifying the best time to change banks and furnish a comprehensive compendium on how to switch banks seamlessly.

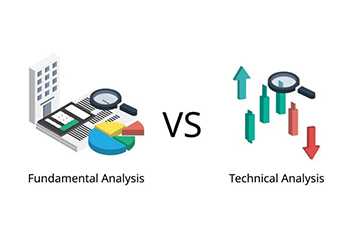

Investing in the stock market can be intimidating, especially with the myriad strategies available. Two of the most popular methods are fundamental analysis and technical analysis. Each approach has unique strengths and weaknesses, making them suitable for different types of investors and market conditions. This article will help you understand when to use fundamental analysis versus technical analysis, making your investment decisions more informed and strategic.

When owning a mobile home, securing a reliable insurance policy is indispensable. A mobile home insurance guide can assist you in navigating the intricacies of coverage options, ensuring you obtain the paramount protection for your investment. This article elucidates what to expect from a good mobile home insurance policy, accentuating key features and considerations to ensure you find the best mobile home coverage.

Estate planning constitutes an imperative stratagem that ensures your assets are administered and apportioned conforming to your predilections posthumously. It’s not solely about wealth but also about bequeathing a legacy for future generations. Strategically orchestrating comprehensive estate engineering for progeny perpetuation can facilitate the establishment of an immutable fiscal legacy, engendering both solvency and constancy within your familial lineage.

Seeing a substantial portion of our income being taxed can be disheartening. However, there are legal ways to reduce our tax burdens, and tax deductions are vital in this process. This article simplifies the concept by presenting the top 10 beliefs that can potentially lead to significant tax savings.

An archer aims intently at a target, believing he can shoot gold. Now imagine waves of intrusion targets moving unpredictably in random directions.

The investment cosmos is perpetually in flux, unveiling avant-garde avenues for the discerning investor to probe for potential augmentation. Amongst these emergent trajectories, SPAC investing benefits risks conspicuously stands as an illustrious strategy. SPACs, or Special Purpose Acquisition Companies, epitomize a divergent methodology for entities to transition into public purview, starkly deviating from the quintessential IPO conduit. This treatise ventures into the intricacies of what are SPACs investing, furnishes a SPAC investment guide, and lucidly expounds on the multifaceted advantages and vicissitudes concomitant with this investment paradigm.

Stock is a great way to earn more money, but it can give people the jitters because of risk. Do not be afraid; stock, like a powerful horse, can be tamed if you learn to control the reins.

Are you looking to buy a new home but want to avoid getting enough money for a down payment?

Hey there, fellow real estate enthusiasts! If you're diving deep into properties and homes, you know that tax time can be a sweet deal or a headache. Lucky for you, the real estate game comes with some neat tax breaks. Let's dive into the top tax breaks every real estate professional should know about.

Navigating the world of student loans can feel like a complex puzzle, especially when juggling other life responsibilities. But fear not! With a blend of savvy strategies and a dash of determination, you can master managing your student loan debt. This guide shares the best tips to come out on top when managing your finances and having a debt-free career after your studies.

Whole life insurance, a permanent life insurance, is particularly advantageous for families looking for long-term financial security. Whole life insurance for families offers the dual benefits of a death benefit and a cash value component, which can be a financial safety net over the years. Families often consider this type of policy when seeking secure, long-lasting financial protection.

In today's dynamic work environment, employee benefits have become a critical factor in attracting and retaining top talent. One such benefit that often holds a significant value is employee stock options (ESOs). If you find yourself with this unique opportunity, it's crucial to understand how to maximize its potential.

Umbrella insurance serves as extra liability protection beyond what regular insurance policies for homes, cars, or boats offer. It kicks in when the coverage limits of your primary insurance policies are used up. This insurance is vital for those facing significant legal claims exceeding their current insurance limits. It offers a crucial financial safeguard, helping to cover substantial liability expenses.

In today's rapidly evolving landscape, technology is a pivotal force driving transformative changes within the insurance sector. This article delves into the profound impact of technology, encompassing innovative insurtech solutions and digital advancements, and how these developments fundamentally reshape the landscape of insurance services. These changes benefit policyholders and insurers, ushering in an era of enhanced efficiency and personalization in insurance operations and offerings.

Engaging in stock market ventures presents an exciting voyage teeming with prospects. Yet, it also unfolds a trail fraught with possible traps that can test the mettle of even experienced traders. Whether you're a financial veteran or just beginning to explore the world of investments, understanding and sidestepping common mistakes is essential to safeguard your financial assets.

For many beginners, choosing the right app can be daunting. But don't worry, you're not alone. We all have different preferences, needs, and aspirations. Maybe you're looking for automation, vast investment options, or just a simple platform to test the waters. We've got you covered.

Being a parent means dreaming big for our kids, and a big part of that dream is giving them a good education.Recent times, like the challenges the Corona phase brought, have shown us how important it is to be ready for anything. The cost of schooling is going up, but it’s an investment we need to make for our kids' future.

Have you ever checked your bank balance at the end of the month and wished you saved more? Many of us find it tough to save after we pay our bills and take care of other needs.Thinking about the future can be a mix of fun and stress. Maybe you dream of buying a new gadget, going on a nice trip, or just having some extra cash. But right now, bills and daily expenses might be in the way.

Handling money can be tricky, almost like trying to walk without tripping. One small mistake can lead to big money problems. Sometimes, we don’t even realize we’re making these mistakes. What happens then? Lower credit scores, arguments with friends or family about money, and a lot of stress. But don't worry too much. You’re not the only one facing these challenges.

Ever had a surprise bill or unexpected repair cost? It's like a bolt from the blue, right? Many of us have been there. But here's something shocking: about a third of Americans don't have extra money set aside for these surprise expenses. This means when something unexpected happens, they might have to use credit cards, get loans, or even dip into their retirement money.

Ever felt like you're working super hard and wondered if your paycheck reflects all that effort? Many of us think about asking for a raise but are scared to take the step. We worry: What if my boss thinks I'm being greedy? What if things get awkward at work? It's natural to feel this way, but here's the thing: if you're working hard and adding value, it's okay to want a fair pay for it.

Ever get emails saying you've won a lottery you never entered or text messages from a bank you don't have an account with? The online world is filled with these tricky messages, trying to fool you into giving away your money or personal info.

Ever found yourself fumbling through your wallet or purse at checkout, scanning for a credit card or cash? Do you still receive paper bank statements in the mail? Isn't it time you moved to something less cumbersome and more secure?

Ever wondered what separates financially successful people from the rest of us? The answer lies in their habits. Financially successful individuals have specific routines and practices that help them build wealth.

Have you ever thought about how your credit card can be both a friend and a foe? For many of us, credit cards are a handy way to pay for things. They’re like a wallet that can offer cool perks when used wisely. But if not careful, they can also lead to debt troubles.

No matter how much you plan or work hard to save, you never know when something uncontrollable will happen and you have nothing with you. Natural disasters, market crashes, inflation, pandemic, and accidents are such uncertainties in our lives. Insurance is one stable factor that can help us get back on our feet with their support policies if such happens. Even the policy you may have chosen might not be perfect; therefore, many recommend getting umbrella insurance. If you are new to this and want the best advice, continue reading and learning more.

Insurance is a way of protecting yourself and your assets from unexpected losses or damages. It can help you cover the costs of medical bills, repairs, lawsuits, or other expenses that may arise from unforeseen events. But how do you choose the right insurance policy for your needs? And how do you make sure you are getting the best value for your money?

Monetary arrangements are now a crucial part of securing our future and achieving our long-term objectives in today's fast-paced world. While there are many tools and techniques for managing money well, indemnity stands out as a key component of any thorough monetary plan. In this article, we will examine how using indemnity can improve monetary arrangements and give you a clear understanding of its importance and advantages.

Roaming around is more than just a pastime for world adventure-seekers; it is a way of life. The thrilling adventure includes discovering new places, experiencing various cultures, and making lifelong memories. But in addition to the excitement of travel, there are dangers and unknowns. Unexpected events can ruin even the best-laid travel plans, from flight delays and lost luggage to medical emergencies abroad.

In today's fast-paced world, managing insurance policies on the go has become more important than ever. With the rise of smartphones and mobile technology, insurance apps have emerged as convenient tools to help individuals handle their policies effortlessly.

Over time, the insurance industry has grown and is still growing with each and every passing day. However, these ten upcoming insurance trends are expected to shake up the entire industry even more.

Getting an insurance policy to secure various aspects of your life is a smart move. However, what is also important is to understand your insurance policy through and through entirely. Many times, while opting for insurance, people blatantly sign away the papers. This is not the right thing to do.

Indemnity is an essential part of financial planning because it shields people and businesses from foreseeable threats. But paying indemnity can be a sizable financial burden. In this article, we will look at ten practical methods for reducing threats and raising indemnity rates without sacrificing coverage. By adhering to these rules, you can safeguard your finances, property, and well-being without sacrificing security or coverage quality.

There is no denying that insurance is a secure way to enter a more financially stable and secure future. However, as great as your decision to start insurance is made, you know this is only one aspect you should be considering. You heard us right.

We all start insurance to support us during unforeseen circumstances, hoping they never come through. However, Murphy’s law has unique timing, and it does pop out sooner or later for some people.

Getting life insurance is one of the best decisions you can make for yourself, and if you have gotten to this point, congratulations! However, as great as this step is, do you know that you cannot hop onto the first insurance company you find online to make a deal with? Yes! Purchasing life insurance while is a great move. It also involves asking yourself many questions to make sure you are making the correct decision.